In our first blog, we focused on awareness and understanding where your money actually goes. Now we are moving to action: designing a forward-looking plan. Designing that plan requires clear alignment between intention and behavior. Before building that plan, two foundational elements must be addressed: your emergency fund and your approach to credit cards.

Emergency Funds: Preparing for the Inevitable

Building an emergency fund is not pessimism; it is preparation. It is insurance against an expense that is unexpected but also inevitable, frequently occurring at the worst possible moment. Preparation requires the willingness to confront uncomfortable possibilities and plan proactively rather than react emotionally. Most people are not ready for this expense. A U.S. Federal Reserve survey in 2024 found that 37% of Americans would need to borrow money or sell something to cover an unexpected $400 expense. This percentage varies with education (18% if you have higher education) and age (53% if you are 18-29 years of age). Financial fragility is more common than we assume.

The purpose of an emergency fund is to provide breathing room. The financial space needed to make sound decisions during stressful periods. Research on financial scarcity shows that cognitive performance declines under economic stress. In one study[1] performance dropped by 13 IQ points, equivalent to a sleepless night, during periods of financial strain. Scarcity narrows decision-making capacity precisely when clarity is most needed. If you unexpectedly lose your employment but have an emergency fund that covers your critical expenses for the next three months, you will likely make better decisions regarding your next steps, and avoid making other bad choices, such as resorting to high interest loans or credit cards.

How large should an emergency fund be? The answer depends on whether you have stable or variable income. If your income is stable, target three months of essential expenses. If your income is variable, consider six months. The objective is not perfection, it is resilience. You should also make sure you keep the emergency funds in a safe and accessible place. This generally means a savings or money-market account with a financial institution. Emergency funds should be held in safe, liquid accounts, typically savings or money market accounts. This is not capital looking for optimal returns. It is capital reserved for stability. If you wish further guidance on savings instruments, you can refer to FDIC resources.

Behavioral barriers often prevent people from building emergency funds. Optimism bias (“nothing will happen”), competing goals, and the friction of repeated decision-making all undermine consistency. We have already addressed the need to see saving for an emergency as precautionary, not negative. We have also explained that these savings occur after essential expenses are covered, so other competing goals can be postponed or adjusted. The best way to address the third obstacle is automation. Schedule transfers on payday from checking to savings. Remove willpower from the equation.

- Credit Cards: Useful Tool or a Source of Risk?

Credit cards are not the villain. They provide convenience, fraud protection, and, when managed responsibly, help build credit history and improved credit scores[2] that help us save on future financing costs when we borrow for a home purchase or other need. The problem begins when credit cards replace savings. When short-term convenience substitutes for long-term structure, the result is often avoidable financial stress. If you do not have a budget, then you may end up spending more than you can afford. If you have not saved money for an emergency fund, then you may end up using your credit card to cover the gap. You will likely be unable to pay your credit card balance and so will pay the minimum credit card payment possible, which adds large financing costs to your existing affordability problem. Remember that minimum payments are designed to extend repayment, not eliminate it efficiently. Credit cards are very expensive sources of funding that are also easily available, which is why it is so common for many of us to get into trouble with credit card debt.

If you carry credit card debt, prioritize paying more than the minimum required payment. For example, A recent news article indicated that paying only the minimum on a $10,000 balance charged at 21.91% interest can stretch repayment to 11 years! Credit card companies maximize their earnings by stretching payments as long as possible, which is why the monthly payments are designed to feel relatively small and manageable. The fees behind this manageability are hidden. For the $10,000 debt, making minimum 2% outstanding balance payments will mean that, in addition to the original debt of $10,000, you will end up paying approximately $17,000 of interest charges. Credit cards also tend to charge late fees that are as high as lawfully permitted. In essence, what is being exploited is another human bias, salience bias, which makes us focus more on what is obvious (the visible monthly payment) rather than the total cost. Otherwise, would any of us accept paying $27,000 for a $10,000 debt?

Even when balances are paid on time, high credit utilization can negatively affect credit scores. Using more than 30% of available credit is generally viewed less favorably. According to myFICO, credit utilization accounts for approximately 30% of your overall credit score. So why should you care about your credit score? Over time, credit score differences can considerably affect borrowing costs. According to American Financing, a good (760) credit score will pay almost $90,000 less in interest compared to a borrower with lower (620-639) credit score on a $250,000, 30-year mortgage loan.

Properly framed, credit cards are transactional tools, not bridges to sustain recurring deficits or lifestyle inflation. Used correctly, they support financial discipline; used passively, they undermine it. For this last point, keep in mind that we should never spend today based on what we are hoping for (but unsure if) we will receive tomorrow.

- Putting It All Together

Now it’s time to move from awareness to action and construct a forward-looking budget. Assuming you have stable income, start by identifying the critical monthly expenses that must be financed to allow you to cover your housing, utility and basic needs. Once you do this, we multiply the value times three (three months of critical needs) to determine your emergency fund. Suppose your essential monthly expenses total $2,500. A three-month buffer implies $7,500. If your goal is to reach that level within two years, you would need to save approximately $312 per month ($7,500 divided by 24 months) or about $78 per week. The same approach can be used to start funding your home or retirement savings once you achieve the first goal of having an emergency fund.

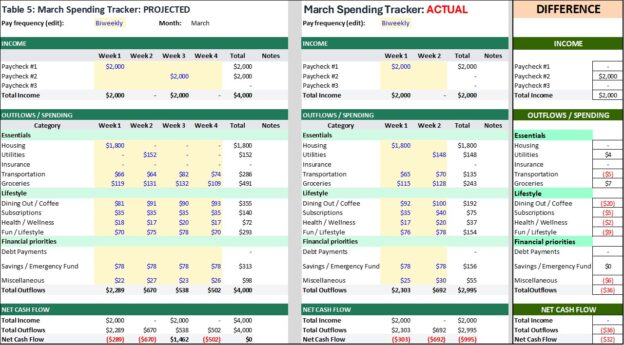

The March “PROJECTED” tab now reflects this plan. Historical patterns from January and February inform the projections, adjusted where appropriate for seasonality. For example, heating costs are lower as spring approaches, so the January and February monthly heating costs may not be a good reflection of what you should expect for this month. A better approximation is same month last year plus any price increases in, say, gas or oil. Notice that you have already incorporated the $78 weekly savings needed to achieve your goal in two years. Notice how rent and utilities appear early in the month, generating negative cash flow of $963 (291+ 672) in Weeks 1 and 2. This is not failure, it is timing. As you do not have any savings, this deficit can be covered through sources such as your credit card, if the surplus funds in the second half of the month are used to pay the credit card debt down. By the end of the month, the Total Net Cash Flow is -$8, meaning you need to reduce your planned expenses for the month by $8 to meet your goals. Assume that you decide to adjust (reduce) your “Dining Out/Coffee” projected expenses by the $8.

Once you adjust your budgeted expenses according to your goals, your new projected budget for March looks as shown in Table 5 (notice the changes in the Dining out/Coffee line). Implementation begins by recording actual spending in the template titled ACTUAL and comparing it against projections. This is where discipline becomes measurable. Notice that, further right, there is a table titled DIFFERENCE. The “DIFFERENCE” column quantifies deviation. Negative values indicate overspending relative to plan; positive values reflect savings. For purposes of this Blog, although the template is designed to show differences in monthly totals, Table 5 shows the differences between our planned and actual spending during week 1 and week 2 to make it easier for the reader. The results should force us to make hard choices.

Weeks 1 and 2 show larger deficits than the projected -$289 and -$670. They are actually -$303 and -$692. There is no going back and adjusting these numbers. This is what has already happened, and it risks derailing your budgeted plan The DIFFERENCE column shows most categories in red, with a cumulative difference of -$32. The response should not be frustration, it is recalibration. Spending in weeks 3 and 4 must compensate. Budgeting is iterative. Note, in DIFFERENCE, that the $32 deficit is largely explained by the deviations in Dining Out/Coffee and Fun/Lifestyle, both totaling -$29 (-$20 + -$9). If you can adjust and reduce your projected spending for weeks 3 and 4 by $32, these will serve you as a guardrail during your actual spending during the last half of March. This process is repeated for the remaining months.

![]()

- Remember, Saving Is the Result of a System, and Not a Personality Trait

Savings success is not a matter of discipline, intelligence or being “good with money”. It is the result of good process that essentially makes savings inertial. This means:

- Automating transfers.

- Scheduling savings deposits/transfers on payday, not at end of month.

- Separating saving and spending accounts.

- Increasing savings as income rises.

- Keep emergency savings untouched, protected from casual use.

Your Future Empowered

Financial well-being is not built with a single decision. It is built in several layers. In the first blog, we focused on awareness. In other words, understanding where your money goes as well as identifying the gaps that create stress. In this second blog, we added a layer of protection and implementation by building buffers, managing credit responsibly, and turning our intentions into action. Together, these steps form a system, and systems can be very empowering. They absorb shocks, reduce uncertainty, and expand options. Wealth can be your long-term financial aspiration. Stability, however, is a design choice that you can begin implementing immediately.

[1] Mani, A., Mullainathan, S., Shafir, E., & Zhao, J. (2013). Poverty impedes cognitive function. Science, 341(6149), 976–980. https://www.science.org/doi/10.1126/science.1238041?utm_source=chatgpt.com

[2] A credit score is a three-digit number, usually ranging from 300 to 850, that predicts how likely you are to repay debt on time. This allows lenders to assess your risk and determine whether you are eligible for a loan.